Posted on

December 31, 2022

by

Marie Taverna

While home prices in many real estate markets across Canada have recorded modest declines over the last few quarters, largely due to the rising cost of borrowing, the rate of decline has slowed. With the expectation that the Bank of Canada’s interest rate hike campaign is coming to a close, Royal LePage is forecasting that the national aggregate price of a home in the fourth quarter of 2023 will be $765,171, 1.0% below Q4 of 2022. Broken out by housing type, the median price of a single-family detached property and condominium are projected to decrease 2.0% and increase 1.0% to $781,256 and $568,933, respectively.

“After nearly two years of record price appreciation, fueled by a steep climb in household savings, very low borrowing costs and an overwhelming desire for more space during the COVID-19 pandemic, the frenzied housing market overshot and the inevitable downward slide or market correction began, intensified by rapidly rising borrowing rates,” said Phil Soper, president and CEO, Royal LePage. “In an era characterized by the unusual, this correction has not followed historical patterns. While the volume of homes trading hands has dropped steeply, home prices have held on, with relatively modest declines. We see this as a continuing trend.”

In the first quarter of 2023, the national aggregate home price is expected to decline on both a year-over-year and quarter-over-quarter basis, followed by near-flat quarterly price growth in Q2. In the second half of next year, the aggregate home price is expected to see modest quarterly gains, but will still remain lower than the same periods in 2022.

The recovery is not expected to be evenly distributed. Regional markets that saw more moderate price growth during the pandemic real estate boom are expected to experience more modest declines. Due to their relative affordability, cities like Calgary, Edmonton and Halifax are expected to record modest price gains in 2023, as they continue to attract out-of-province buyers, especially first-time homebuyers from southern Ontario and British Columbia looking for more affordable housing.

Read Royal LePage’s 2023 Market Survey Forecast for national and regional insights.

Highlights from the release:

- Condominium prices are expected to outdo single-family homes in all major markets across Canada, except Edmonton and Winnipeg

- The Greater Toronto Area and Greater Montreal are expected to see a Q4 2023 aggregate price decline of 2.0% year-over-year

- The Q4 2023 aggregate home price in Greater Vancouver is anticipated to decrease 1.0% year-over-year

- Despite declining affordability, heightened by rising interest rates, continued housing supply shortage acts as a floor on home price declines

Posted on

November 18, 2022

by

Marie Taverna

Backgrounder

In Budget 2022, the government proposed the introduction of the Tax-Free First Home Savings Account (FHSA). This new registered plan would give prospective first-time home buyers the ability to save $40,000 on a tax-free basis. Like a Registered Retirement Savings Plan (RRSP), contributions would be tax-deductible, and withdrawals to purchase a first home—including from investment income—would be non-taxable, like a Tax-Free Savings Account (TFSA).

Budget 2022 announced the key design features of the FHSA, including an $8,000 annual contribution limit in addition to a $40,000 lifetime contribution limit. Today, the Department of Finance is releasing for public comment draft legislative proposals that provide additional details on the design of the FHSA. This backgrounder offers a summary of these details.

The government expects that Canadians will be able to open and contribute to an FHSA at some point in 2023. No matter when this happens in 2023, Canadians would be allowed to contribute the full $8,000 annual limit in that year.

Opening and Closing Accounts

To open an FHSA, an individual must be a resident of Canada and at least 18 years of age. In addition, an individual must be a first-time home buyer, meaning that they have not owned a home in which they lived at any time during the part of the calendar year before the account is opened or at any time in the preceding four calendar years. For this purpose, ownership is defined broadly and includes beneficial ownership, but excludes a right to acquire less than 10% of a qualifying home.

An FHSA of an individual would cease to be an FHSA, and the individual would not be permitted to open an FHSA, after December 31 the year in which the earliest of these events occurs:

- The fifteenth anniversary of the individual first opening an FHSA; or

- The individual turns 71 years old.

Any savings not used to purchase a qualifying home could be transferred on a tax-free basis into an RRSP or Registered Retirement Income Fund (RRIF) or would otherwise have to be withdrawn on a taxable basis. Individuals that make a qualifying withdrawal could transfer any unwithdrawn savings on a tax-free basis to an RRSP or RRIF until December 31 of the year following the year of their first qualifying withdrawal.

Qualified Investments

An FHSA would be permitted to hold the same qualified investments that are currently allowed to be held in a TFSA. In particular, taxpayers would be able to hold a broad range of investments, including mutual funds, publicly traded securities, government and corporate bonds, and guaranteed investment certificates.

The prohibited investment rules and non-qualified investment rules applicable to other registered plans would apply, including the potential tax consequences described below. These rules are intended to disallow investments in entities with which the account holder does not deal at arm's length, as well as investments in certain assets such as land, shares of private corporations and general partnership units.

Contributions

The lifetime limit on contributions would be $40,000, with an annual contribution limit of $8,000. In other words, individuals would be subject to the lesser of their annual limit and remaining lifetime limit. The full annual limit would be available starting in 2023.

The annual contribution limit would apply to contributions made within a particular calendar year. Individuals would be able to claim an income tax deduction for contributions made in a particular taxation year. Unlike RRSPs, contributions made within the first 60 days of a given calendar year could not be attributed to the previous tax year.

An individual would be allowed to carry forward unused portions of their annual contribution limit up to a maximum of $8,000. This means that an individual contributing less than $8,000 in a given year could contribute the unused amount (i.e., $8,000 less their contribution in that year) in a subsequent year on top of their annual contribution limit of $8,000 (subject to their lifetime contribution limit). For example, an individual contributing $5,000 to an FHSA in 2023 would be allowed to contribute $11,000 in 2024 (i.e., $8,000 plus the remaining $3,000 from 2023). Carry-forward amounts would only start accumulating after an individual opens an FHSA for the first time.

An individual would be permitted to hold more than one FHSA, but the total amount that an individual contributes to all of their FHSAs could not exceed their annual and lifetime contribution limits. Taxpayers would generally be responsible for ensuring they do not exceed their limit in a given year. The Canada Revenue Agency (CRA) would provide basic FHSA information to support taxpayers in determining how much they can contribute in a given year.

Contributions made to an FHSA following a qualifying withdrawal being made (i.e., when buying a first home) would not be deductible from net income.

Undeducted Contributions

An individual would not be required to claim a deduction for the tax year in which a contribution is made. Like RRSP deductions, such amounts could be carried forward indefinitely and deducted in a later tax year.

Qualifying Withdrawals

In order for an FHSA withdrawal to be a qualifying (i.e., non-taxable) withdrawal, certain conditions must be met.

First, a taxpayer must be a first-time home buyer at the time a withdrawal is made. Specifically, the taxpayer could not have owned a home in which they lived at any time during the part of the calendar year before the withdrawal is made or at any time in the preceding four calendar years. There is an exception to allow individuals to make qualifying withdrawals within 30 days of moving into their home.

The taxpayer must also have a written agreement to buy or build a qualifying home before October 1 of the year following the year of withdrawal and intend to occupy the qualifying home as their principal place of residence within one year after buying or building it.

A qualifying home would be a housing unit located in Canada. A share in a co-operative housing corporation that entitles the taxpayer to possess, and have an equity interest in a housing unit located in Canada, would also qualify. However, a share that only provides a right to tenancy in the housing unit would not qualify.

Provided the taxpayer meets the qualifying withdrawal conditions, the entire amount of available FHSA funds may be withdrawn on a tax-free basis in a single withdrawal or a series of withdrawals.

Non-qualifying Withdrawals

Withdrawals that are not qualifying withdrawals would be included in the income of the individual making the withdrawal. Financial institutions would be required to collect and remit withholding tax on non-qualifying withdrawals, consistent with the treatment applicable to taxable RRSP withdrawals.

Non-qualifying withdrawals would not re-instate either the annual contribution limit or the lifetime contribution limit.

Transfers

An individual could transfer funds from an FHSA to another FHSA, an RRSP or a RRIF on a tax-free basis.

Funds transferred to an RRSP or RRIF will be subject to the usual rules applicable to these accounts, including taxability upon withdrawal. These transfers would not reduce, or be limited by, an individual's available RRSP contribution room. These transfers would not reinstate an individual's FHSA lifetime contribution limit.

Individuals would also be allowed to transfer funds from an RRSP to an FHSA on a tax-free basis, subject to the FHSA annual and lifetime contribution limits and the qualified investment rules. Although such transfers would be subject to FHSA contribution limits, they would not be deductible and would also not reinstate an individual's RRSP contribution room.

Treatment of FHSA Income for Tax and Income-Tested Benefit Purposes

Contributions to an FHSA would be deductible in computing income for tax purposes. In addition, income, losses and gains in respect of investments held within an FHSA, as well as qualifying withdrawals, would not be included (or deducted) in computing income for tax purposes or taken into account in determining eligibility for income-tested benefits or credits delivered through the income tax system (for example, the Canada Child Benefit and the Goods and Services Tax Credit).

Eligible Issuers

Any financial institution that is able to issue RRSPs and TFSAs would be able to issue FHSAs. This includes Canadian trust companies, life insurance companies, banks and credit unions.

Interaction with the Home Buyers' Plan (HBP)

The HBP would continue to be available as under existing rules. However, an individual would not be permitted to make both an FHSA withdrawal and an HBP withdrawal in respect of the same qualifying home purchase.

Spousal Contributions and Attribution Rules

The FHSA holder would be the only taxpayer permitted to claim deductions for contributions made to their FHSA. Individuals would not be able to contribute to their spouse or common-law partner's FHSA and claim a deduction.

That said, an individual could contribute to their FHSA from funds provided to them by their spouse. Normally, if an individual transfers property to the individual's spouse or common-law partner, the income tax rules generally treat any income earned on that property as income of the individual. An exception to these "attribution rules" would allow individuals to take advantage of the FHSA contribution room available to them using funds provided by their spouse. Specifically, these attribution rules would not apply to income earned in an FHSA that is derived from such contributions.

Marital Breakdowns

On the breakdown of a marriage or a common-law partnership, it is proposed that an amount may be transferred directly from the FHSA of one party to the relationship to an FHSA, RRSP, or RRIF of the other. In such circumstances, transfers would not re-instate any contribution room of the transferor, and would not be counted against any contribution room of the transferee.

Over-contribution, Non-qualified Investment, Prohibited Investment, and Advantage Taxes

Like TFSAs, a 1% tax on over-contributions to an FHSA would apply for each month (or a part of a month) to the highest amount of such excess that exists in that month.

When a taxpayer's annual contribution limit is reset at the beginning of each calendar year, over-contributions from a previous year may cease to be an over-contribution. A taxpayer would be allowed to deduct an over-contributed amount for a given year in the tax year in which it ceases to be an over-contribution but not earlier. However, if a qualifying withdrawal is made before an over-contribution ceases to be an over-contribution, no deduction would be provided for the over-contributed amount.

Example:

Alyssa contributes $10,000 on November 15, 2023 and does not withdraw it. This contribution exceeds Alyssa's annual FHSA contribution limit by $2,000.

Alyssa would be subject to an over-contribution tax of $40 (1% × $2,000 × 2 months) when filing her 2023 tax return in 2024. The $2,000 amount would cease to be an over-contribution on January 1, 2024, as a new annual limit of $8,000 would be available.

Alyssa would be allowed to deduct $8,000 from her 2023 net income. Presuming Alyssa did not make a qualifying withdrawal between November 15, 2023 and January 1, 2024, she would be allowed to deduct the additional $2,000 from her 2024 net income.

The Income Tax Act imposes other taxes in certain circumstances involving non-qualified investments, prohibited investments, and unintended advantages in respect of other registered plans. These rules would also apply to the FHSA.

The Minister of National Revenue would have authority to cancel or waive all or part of these taxes in appropriate circumstances. Various factors would be taken into account including reasonable error, the extent to which the transactions that gave rise to the tax also gave rise to another tax, and the extent to which payments were made from the taxpayer's registered plan.

Treatment Upon Death

Like TFSAs, individuals would be permitted to designate their spouse or common-law partner as the successor account holder, in which case the account could maintain its tax-exempt status. If named as the successor holder, the surviving spouse would become the new holder of the FHSA immediately upon the death of the original holder provided the surviving spouse meets the eligibility criteria to open an FHSA (see the discussion above under "Opening and Closing Accounts"). Inheriting an FHSA in this way would not impact the surviving spouse's contribution limits. Inherited FHSAs would assume the surviving spouse's closure deadlines. If the surviving spouse is not eligible to open an FHSA, amounts in the FHSA could instead be transferred to an RRSP or RRIF of the surviving spouse, or withdrawn on a taxable basis.

If the beneficiary of an FHSA is not the deceased account holder's spouse or common-law partner, the funds would need to be withdrawn and paid to the beneficiary. Amounts paid to the beneficiary would be included in the income of the beneficiary for tax purposes. When such payments are made, the payment to the beneficiary would be subject to withholding tax.

Non-residents

Taxpayers would be allowed to contribute to their existing FHSAs after emigrating from Canada, but they would not be able to make a qualifying withdrawal as a non-resident. Specifically, a taxpayer withdrawing funds from an FHSA must be a resident of Canada at the time of withdrawal and up to the time a qualifying home is bought or built.

Withdrawals by non-residents would be subject to withholding tax.

Reporting Requirements

Opening an Account

In order to open an FHSA, a taxpayer would be required to confirm their eligibility to an eligible issuer.

Ongoing Reporting

Financial institutions would be required to send to the CRA annual information returns in respect of each FHSA that they administer. The CRA would use information provided by issuers to administer the FHSA and provide basic FHSA information to taxpayers.

Withdrawals

In order to make a qualifying withdrawal, an individual would be required to submit a request to their FHSA issuer confirming their eligibility. Issuers would not apply withholding taxes upon receiving a valid qualifying withdrawal request.

When any withdrawals are made (qualifying or non-qualifying), the FHSA issuer would be required to prepare an information slip with the amount of the withdrawal and, in the case of a non-qualifying withdrawal, any income tax withheld on that amount.

Account Closure

The CRA would issue a reminder to all taxpayers and their FHSA issuers of when an FHSA will no longer have tax-advantaged status.

Deposit Insurance Framework

The Canada Deposit Insurance Corporation insures eligible deposits up to $100,000 per member institution, per person, per category. It is proposed that the Canada Deposit Insurance Corporation Act be amended to create a new category of insured deposits for FHSAs, as is the case for RRSPs and TFSAs.

Interest Deductibility

Like RRSPs and TFSAs, interest on money borrowed to invest in an FHSA would not be deductible in computing income for tax purposes.

Collateralization

Taxpayers must include in income the full value of any assets held within an FHSA and pledged as collateral for a loan.

Bankruptcy

FHSAs would not be afforded creditor protection under the Bankruptcy and Insolvency Act.

Posted on

November 8, 2022

by

Marie Taverna

Inflation, rising interest rates create caution across Metro Vancouver’s housing market

Home sale activity across the Metro Vancouver housing market continued to trend well below historical averages in October.

The Real Estate Board of Greater Vancouver (REBGV) reports that residential home sales in the region totalled 1,903 in October 2022, a 45.5 per cent decrease from the 3,494 sales recorded in October 2021, and a 12.8 per cent increase from the 1,687 homes sold in September 2022.

Last month’s sales were 33.3 per cent below the 10-year October sales average.

“Inflation and rising interest rates continue to dominate headlines, leading many buyers and sellers to assess how these factors impact their housing options,” Andrew Lis, REBGV’s director, economics and data analytics said. “With sales remaining near historic lows, the number of active listings continues to inch upward, causing home prices to recede from the record highs set in the spring of 2022.”

There were 4,033 detached, attached and apartment properties newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in October 2022. This represents a 0.4 per cent decrease compared to the 4,049 homes listed in October 2021 and a 4.6 per cent decrease compared to September 2022 when 4,229 homes were listed.

The total number of homes currently listed for sale on the MLS® system in Metro Vancouver is 9,852, a 22.6 per cent increase compared to October 2021 (8,034) and a 1.2 per cent decrease compared to September 2022 (9,971).

“Recent years have been characterized by a frenetic pace of sales amplified by scarce listings on the market to choose from. Today’s market cycle is a marked departure, with a slower pace of sales and more selection to choose from,” Lis said. “This environment provides buyers and sellers more time to conduct home inspections, strata minute reviews, and other due diligence. With the possibly of yet another rate hike by the Bank of Canada this December, it has become even more important to secure financing as early in the process as possible.”

For all property types, the sales-to-active listings ratio for October 2022 is 19.3 per cent. By property type, the ratio is 14.3 per cent for detached homes, 21.6 per cent for townhomes, and 23.2 per cent for apartments.

Generally, analysts say downward pressure on home prices occurs when the ratio dips below 12 per cent for a sustained period, while home prices often experience upward pressure when it surpasses 20 per cent over several months.

The MLS® Home Price Index composite benchmark price for all residential properties in Metro Vancouver is currently $1,148,900. This represents a 2.1 per cent increase from October 2021, a 9.2 per cent decrease over the last six months, and a 0.6 per cent decrease compared to September 2022.

Sales of detached homes in October 2022 reached 575, a 47.2 per cent decrease from the 1,090 detached sales recorded in October 2021. The benchmark price for detached properties is $1,892,100. This represents a 1.6 per cent increase from October 2021 and a 0.7 per cent decrease compared to September 2022.

Sales of apartment homes reached 995 in October 2022, a 44.8 per cent decrease compared to the 1,801 sales in October 2021. The benchmark price of an apartment property is $727,100. This represents a 5.1 per cent increase from October 2021 and a 0.2 per cent decrease compared to September 2022.

Attached home sales in October 2022 totalled 333, a 44.8 per cent decrease compared to the 603 sales in October 2021. The benchmark price of an attached unit is $1,043,600. This represents a 7.1 per cent increase from October 2021 and a 0.5 per cent decrease compared to September 2022.

Download the October 2022 stats package.

Posted on

October 13, 2022

by

Marie Taverna

Basements are often an afterthought. Sometimes they’re dismissed as simply storage space – where your furnace and water heater are located, along with bins of clothes you’ll never wear again. If this is your mindset, you’re missing out on some great opportunities to reimagine this space.

See your basement with a fresh perspective. Here are a few ways that you can optimize your basement for a better living experience:

Personal gym

Forget paying for a membership. By investing in a few pieces of quality gym equipment, you can bring your workout home. It’s not always easy to stay motivated, but having easy access to your treadmill at home could be one less excuse to skip your run, especially on those cold days. And with a home gym, you can make exercise time a part of your family’s routine.

Playroom

If you have children, you know how quickly their toys can take over a room. By making the basement (or part of it) a dedicated play area, you can keep the clutter out of sight downstairs while giving the kids plenty of room for imaginative games and activities. Add a fresh coat of paint, a few whimsical decals and the toys of course, and you’ll have a playroom that dreams are made of.

Home theatre

With so many movies available on streaming platforms, trips to the cinema have become rare. But, you can recreate the experience at home with a large screen, projector, and theatre-style armchairs. For those with smaller basements, a quality flatscreen TV and a comfortable couch with lots of pillows can be just as enjoyable for family movie nights or entertaining friends.

Library

For all the book lovers out there, imagine having a special place to read, with all the paperbacks you’ve collected over the years at your fingertips. Whether it’s a few bookshelves and some comfy seating, or custom built-ins that showcase your collection in a creative way – a library is a wonderful addition to any home. Coordinating rugs, throws, and cushions can give this space a luxe yet cozy feel. It’s the perfect place to get lost in a good book!

Home office

Maybe the kitchen table isn’t cutting it. For some, working from home is now part of the regular routine but many still don’t have a dedicated home office. A well-designed workspace with an ergonomic desk and chair can not only increase your productivity and help motivate you to check off your daily to-dos faster, it can reduce the physical stress that your body endures during long stretches of sedentary activity. And the best part is, you don’t have to clear away your work day each time you sit down for a meal.

Basements are a blank canvas; extra square footage to play with and room to try something new. So, however you decide to use this part of your home, choose something you love and make the space your own!

Posted on

October 13, 2022

by

Marie Taverna

Fall is a beautiful time of year. As the leaves change colour, pumpkin patches open, and people enjoy spiced lattes and sweater weather, it’s only fitting to add a little fall flair to your home as well. And, seasonal décor doesn’t have to be difficult or break the bank.

Just in time for the Thanksgiving long weekend, here are some simple tips to warm up your home and a touch of autumn to your style:

Warm up your front entrance

Adorn the front of your home with fall-inspired welcome mats, wooden crates, and squash in various shapes and sizes. The beauty of fall is that there is no symmetry needed. Scatter different sized boxes, fall signs and a mix of small and large decorative pumpkins (real or fake). Hang a fall wreath made of twigs, and add a brown, orange or burgundy ribbon for a pop of colour.

Decorate your dining space

Beautify your home indoors with orange and earthy tones. Add a table runner, some coloured napkins on the table, and coordinating candles in the scents of the season. You can elevate your seasonal look with small squashes and gourds as centerpieces. And, don’t be afraid to bring the outside in… Design your own table arrangement with twigs, leaves and pine cones you collect.

Add a cookie and coffee station

Nothing says fall like warm beverages and treats while enjoying the crisp air! Impress your guests with a coffee and tea station. Set up cups, specialty teas displayed in a glass bottle, hot coffee and flavoured syrups in a section of your dining room or kitchen. Use risers or wooden trays to give the display some complexity. Add a cookie jar or cake stand with some fall goodies such as butter tarts, chocolate chip cookies, or brownies. You can also have a seasonal fruit basket with apples and pears.

Make it cozy

Celebrate fall with comfort by adding aromatic autumn candles… Think cinnamon, vanilla, pumpkin spice scents. Light them in the evenings for ambiance. Add fall-themed throw cushions, and add an earthy-toned warm blanket on your couch (check out Pinterest for inspiration on how to arrange pillows and blankets).

These simple tricks can elevate your home decor and make it feel as warm as your pumpkin or apple pie this season!

Posted on

October 13, 2022

by

Marie Taverna

Canadian home prices are projected to end the year modestly lower than where they were during the final months of 2021, undoing the price growth seen earlier this year. Royal LePage is forecasting that the aggregate price of a home in Canada will decrease 0.5% in the fourth quarter of 2022, compared to the same quarter last year, due to a continued softening of home prices in a majority of markets across the country in the third quarter (94% of regions in the report).

“September did not bring the typical seasonal lift in the number of homes trading hands in this country, a clear indication that our housing market continues to adjust to higher borrowing costs,” said Phil Soper, president and CEO of Royal LePage. “Home prices follow sales volume trends, which means we will see further softening in the final months of the year. Our revised outlook has national prices at just below where we ended 2021, erasing the gains made in the first quarter of 2022.”

According to the Royal LePage House Price Survey, the aggregate price of a home in Canada increased 3.3% year-over-year to $774,900 in the third quarter of 2022. However, on a quarterly basis, that figure decreased 4.9%; the second consecutive quarterly decline recorded. When broken out by housing type, the national median price of a single-family detached home rose 2.0% year-over-year to $806,100, while the median price of a condominium increased 6.1% year-over-year to $566,100.

With so many would-be buyers waiting on the sidelines, sales activity has weakened across the country.

“While sales volumes are well off the pandemic-fueled peak, many buyers remain active in today’s market. Some are motivated to transact before their locked-in mortgage pre-approval rates expire. Others are encouraged by a rare drop in home prices, the lack of bidding wars and the ability to include conditions in purchase offers,” added Soper. “At the first indication that interest rates have ended their climb and home prices have stabilized, I would expect a sharp increase in those entering the market as the need for housing has not diminished one bit. And regrettably, Canada continues to suffer from a severe shortage of housing supply.”

Read Royal LePage’s third quarter release for national and regional insights.

Third quarter press release highlights:

- National aggregate home price for the final quarter of the year forecast at -0.5%

- National aggregate home price increased 3.3% year-over-year in third quarter of 2022; decreased 4.9% quarter-over-quarter

- Prices remain well above pre-pandemic levels; Canada’s national aggregate home price increased 25.4% in Q3 over the same quarter in 2020, and 21.5% over the same quarter in 2019

- 58 of the report’s 62 regional markets posted quarterly aggregate home price declines in Q3

- Prices decline on a quarterly basis in Greater Montreal Area for the first time in more than five years as market activity drops, following trend set in greater regions of Toronto and Vancouver in Q2

- Major markets in Atlantic Canada and the Prairies show modest quarterly price declines in Q3; Calgary and Edmonton markets faring better than other major cities

Posted on

October 4, 2022

by

Marie Taverna

Fall is now here and it’s time to update porch décor from cheugy to chic! Fall is now here and it’s time to update porch décor from cheugy to chic!

This year we’re thinking tonal, monochromatic elegance. These front porch decorating ideas will surely pique your interest by emphasizing the effortless aesthetic of Canadian contemporary design.

Posted on

October 4, 2022

by

Marie Taverna

|

Metro Vancouver saw more home sellers and fewer buyers in September

Home sellers were more active in Metro Vancouver’s housing market in September while home buyer demand remained below the region’s long-term averages.

The Real Estate Board of Greater Vancouver (REBGV) reports that residential home sales in the region totalled 1,687 in September 2022, a 46.4 per cent decrease from the 3,149 sales recorded in September 2021, and a 9.8 per cent decrease from the 1,870 homes sold in August 2022.

Last month’s sales were 35.7 per cent below the 10-year September sales average.

“With the Bank of Canada and other central banks around the globe hiking rates in an effort to stamp out inflation, the cost to borrow funds has risen substantially over a short period,” said Andrew Lis, REBGV director, economics and data analytics. “This has resulted in a more challenging environment for borrowers looking to purchase a home, and home sales across the region have dropped accordingly.”

There were 4,229 detached, attached and apartment properties newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in September 2022. This represents an 18.2 per cent decrease compared to the 5,171 homes listed in September 2021 and a 27.1 per cent increase compared to August 2022 when 3,328 homes were listed.

The total number of homes currently listed for sale on the MLS® system in Metro Vancouver is 9,971, an eight per cent increase compared to September 2021 (9,236) and a 3.2 per cent increase compared to August 2022 (9,662).

“With fewer homes selling and new listings continuing to come to market, inventory is beginning to accumulate, providing buyers with more selection compared to last year,” Lis said. “With more supply and less demand within this market cycle, residential home prices have edged down in the region over the last six months.”

For all property types, the sales-to-active listings ratio for September 2022 is 16.9 per cent. By property type, the ratio is 12.4 per cent for detached homes, 18.4 per cent for townhomes, and 20.9 per cent for apartments.

Generally, analysts say downward pressure on home prices occurs when the ratio dips below 12 per cent for a sustained period, while home prices often experience upward pressure when it surpasses 20 per cent over several months.

The MLS® Home Price Index composite benchmark price for all residential properties in Metro Vancouver is currently $1,155,300. This represents a 3.9 per cent increase over September 2021, an 8.5 per cent decline over the past six months, and a 2.1 per cent decline compared to August 2022.

Sales of detached homes in September 2022 reached 525, a 44.7 per cent decrease from the 950 detached sales recorded in September 2021. The benchmark price for a detached home is $1,906,400. This represents a 3.8 per cent increase from September 2021 and a 2.4 per cent decrease compared to August 2022.

Sales of apartment homes reached 888 in September 2022, a 45.2 per cent decrease compared to the 1,621 sales in September 2021. The benchmark price of an apartment home is $728,500. This represents a 6.2% per cent increase from September 2021 and a 1.6 per cent decrease compared to August 2022.

Attached home sales in September 2022 totalled 274, a 52.6 per cent decrease compared to the 578 sales in September 2021. The benchmark price of an attached home is $1,048,900. This represents a 9.1 per cent increase from September 2021 and a 1.9 per cent decrease compared to August 2022.

Download the September 2022 stats package.

|

|

Posted on

October 3, 2022

by

Marie Taverna

How has the increased cost of living impacted Canadians' homebuying plans this year?

With interest rates continuing to increase and inflation reaching a decades high, younger Canadians have been especially affected.

Read our latest blog post to learn how many Canadians have been forced to deprioritize their plans to buy a home. Read our latest blog post to learn how many Canadians have been forced to deprioritize their plans to buy a home.

Posted on

September 21, 2022

by

Marie & Kim Taverna

Royal LePage Survey: 3.2 million boomers in Canada considering buying a home within the next five years

Survey Highlights:

According to a recent Royal LePage survey[1] of boomers in Canada, defined by StatsCan as having been born between 1946 and 1965, 35 per cent of the cohort – or approximately 3.2 million boomers[2] – said they are considering a home purchase within the next five years. Nationally, 45 per cent of respondents believe now is a good time to sell their home.

“The boomer generation appears to have no intention of slowing down,” said Phil Soper, President and CEO, Royal LePage. “Fully vaccinated, and turning a cold shoulder to retirement, the typical member of this huge demographic is enjoying an empty nest and believes real estate is a good investment. Millions of boomers are expected to wade into the market over the next five years.”

Boomer Housing Demand

There is no one-size-fits-all outcome as Canadian boomers age into retirement, especially when it comes to their decision about where to live. More than half (57%) of respondents said they would purchase a detached house if they were to buy, while 19 per cent said they would prefer an apartment/condominium. Fifty-two per cent of boomer homeowners said they would prefer to renovate their existing home rather than purchase another, and an additional 24 per cent said they would consider it.

Of the 35 per cent of boomers who say they are considering purchasing a primary residence in the next five years, 56 per cent say they would consider moving to a rural or recreational region. Twenty-eight per cent say they would consider purchasing a larger home than the one they currently reside in, 56 per cent would consider a similarly-sized property, and 63 per cent would consider downsizing. Respondents were able to choose more than one option. The most popular reason for downsizing is less home maintenance (71%). Other popular choices include the ability to free up money for things like retirement (39%), travel (29%), and to help their children purchase a home (9%).

“Turning full circle to those carefree, pre-children years, most boomers are looking for a home that requires less maintenance,” Soper continued. “Paradoxically, they also yearn for country living and don’t want to sacrifice living space. Look for the continued growth of managed communities in exurban and recreational regions.”

Working boomers largely did not consider their region affordable (65%) and 42 per cent said they would consider a move to a different city, near or during retirement.

Since the onset of the COVID-19 pandemic, more than 550,000 Canadian boomers (6%) have sold their homes or are in the process of selling, and at least 90 per cent said the global health crisis neither caused their plans of moving to be postponed nor expedited.

Homeownership and Personal Wealth

Seventy-five per cent of boomers own their own home, the majority of whom do not currently have a mortgage (64%). Seventeen per cent of boomer homeowners own more than one property, and 40 per cent have at least 50 per cent of their net wealth in real estate.

“The boomer generation strongly values home ownership, for good reason. Real estate has been very, very good to them,” said Soper. “Most are still working and their home equity has become the bedrock of retirement security. Financially confident, their next move is a matter of lifestyle choice.”

Seventy-eight per cent of Canadian boomers believe that home ownership is a good investment.

Boomers keep ‘bank of mom and dad’ open

As home prices continue to grow across the country, many young adults are turning to their boomer parents for help with a down payment on a property. Twenty-five per cent of boomers say they have or would consider gifting or loaning money to a child to help with the purchase of a home. In Vancouver, that figure reaches as high as 34 per cent.

“Over the past year, home values have appreciated sharply in virtually every market from coast to coast. Affordability is a major issue for young Canadians and with stricter mortgage stress test measures in place, they must clear higher hurdles,” Soper said. “Many are turning to the so-called ‘bank of mom and dad’ to achieve the dream of home ownership. The parental bank appears willing, even if it means delaying retirement.”

A recent Royal LePage and Sagen survey[3] of first-time homebuyers in Canada found that 62 per cent of respondents nationwide felt anxious about missing out on a property they wanted because of an insufficient down payment, before buying their first home. That figure increased to 75 per cent in Toronto and 69 per cent in Vancouver.

Seventy-nine per cent of Canadian boomers do not have children living in their home. This includes boomers who are not parents. Seventeen per cent of them have adult children living at home. Seven per cent of those surveyed said they have children aged 18 to 24, and 12 per cent said they have children 25 years of age or older living at home.

Of those who have children living at home, 43 per cent plan to stay in their current property once their kids have moved out. Meanwhile, 21 per cent said they do not foresee their children leaving.

By the end of this decade, all boomers will be 65 or older, which typically coincides with retirement in Canada. Twenty-seven per cent of boomers who are currently working said they would consider delaying retirement to help their children with a down payment on a home.

For all regional and national responses, click here: rlp.ca/table_boomersurvey2021

Regional Summaries

Atlantic Canada

Twenty-nine per cent of boomers in Atlantic Canada are considering purchasing a home within the next five years. Seventy-eight per cent of boomers in the Maritimes own their own home, the majority of whom do not currently have a mortgage (72%), which is among the highest rates in Canada.

“The affordability of real estate in Atlantic Canada allows homeowners to pay off their loans quicker and enter retirement mortgage-free,” said Glenn Larkin, sales representative, Royal LePage Vision Realty, in St. John’s, Newfoundland.

Sixteen per cent of boomer homeowners in the region own more than one property, and 21 per cent have at least 50 per cent of their net wealth in real estate. More than two-thirds (67%) of respondents said they would purchase a detached house if they were to buy, while 11 per cent said they would prefer an apartment/condominium.

“Although home prices are more affordable in the Maritimes, some first-time buyers are finding current market conditions challenging, as prices have appreciated at record rates, partially driven by a surge of out-of-province buyers over the last year,” continued Larkin. “Many parents with the ability to do so, are helping their children with a down payment. Often they are using some of the profit from the sale of their own family home.”

Nineteen per cent of respondents in Atlantic Canada are likely to assist, or have assisted, a child financially with the purchase of a home, the lowest rate of all surveyed regions in the country.

Forty-nine per cent of boomer homeowners in Atlantic Canada said they would prefer to renovate their existing home rather than purchase another, and an additional 26 per cent said they would consider it.

For all regional and national responses, click here: rlp.ca/table_boomersurvey2021

Quebec

Twenty-nine per cent of boomers in Quebec are considering purchasing a home within the next five years, which is among the lowest rates in Canada. At 62 per cent, Montreal has the lowest rate of home ownership among boomers. That figure rises to 67 per cent in the province, the majority of whom do not currently have a mortgage (57%). Sixteen per cent of boomer homeowners in Quebec own more than one property, and 34 per cent have at least 50 per cent of their net wealth in real estate.

More than half (53%) of respondents in Quebec said they would purchase a detached house if they were to buy, while 20 per cent said they would prefer an apartment/condominium.

Of the 29 per cent of boomers in Quebec who are considering purchasing a primary residence in the next five years, 62 per cent say they would consider moving to a rural or recreational region. Thirty-two per cent say they would consider purchasing a larger home than the one they currently reside in, 53 per cent would consider a similarly-sized property, and 59 per cent would consider downsizing (55% in Montreal). Respondents were able to choose more than one answer. The most popular reason among Quebec boomers for downsizing is less home maintenance (72%). Other popular choices include the ability to free up money for things like retirement (36%), travel (21%), and to help their children purchase a home (13%). Montreal respondents who are considering to downsize also value the ability to free up money for retirement (41%), travel (21%), and to help their children purchase a home (15%).

“While the expectation may have been that boomers would downsize into condominiums en masse, the proportion of Quebec boomers looking to move into a larger property is among the highest in Canada,” said Georges Gaucher, broker and owner, Royal LePage Village. “Although prices continue to rise in the Belle Province, it remains one of the most affordable markets in the country.”

Twenty-four per cent of respondents in Quebec are likely to assist a child financially with the purchase of a home.

Sixty-two per cent of boomer homeowners in Quebec said they would prefer to renovate their existing home rather than purchase another, among the highest rates of all the regions surveyed. An additional 21 per cent said they would consider it.

“We expect that as COVID-19 safety restrictions continue to be lifted and as the vaccination campaign progresses, some Quebec boomers will put their homes on the market, which will improve inventory selection for potential buyers,” added Gaucher. “However, while the variety of listings will improve, boomers who are selling are also expected to purchase. This will add more competition to the market.”

For all regional and national responses, including Montreal, click here: rlp.ca/table_boomersurvey2021

Ontario

Slightly higher than the national average, 37 per cent of boomers in Ontario are considering purchasing a home within the next five years (41% in Toronto). Seventy-six per cent of boomers in the province own their own home, the majority of whom do not currently have a mortgage (64% and 60% in Toronto). Sixteen per cent of boomer homeowners in the province own more than one property, and 46 per cent have at least 50 per cent of their net wealth in real estate. In Toronto that number reaches 54 per cent, the highest of all census metropolitan areas surveyed.

“The pandemic has left a lasting impact on many younger boomers who are trying to get more from their home after a year of COVID-19 related health restrictions. Many are looking for more space to entertain, help out with the grandkids or continue to work remotely. Not all boomers have the luxury to upgrade to a larger space, but the desire is there,” said Cailey Heaps, who leads the Heaps Estrin Team, Royal LePage Real Estate Services, in Toronto.

More than half (59%) of Ontario boomers said they would purchase a detached house if they were to buy, while 19 per cent said they would prefer an apartment/condominium.

Of the 37 per cent of boomers in Ontario who say they are considering purchasing a primary residence in the next five years, 56 per cent say they would consider moving to a rural or recreational region. Twenty-five per cent say they would consider purchasing a larger home than the one they currently reside in (26% in Toronto), 54 per cent would consider a similarly-sized property (57% in Toronto), and 66 per cent would consider downsizing (59% in Toronto). Respondents were able to choose more than one option. The most popular reason for downsizing is less home maintenance (73%). Other popular choices include the ability to free up money for things like retirement (38%), travel (35%), and to help their children purchase a home (11%). Toronto boomers who are considering to downsize also value the ability to free up money for retirement (49%), travel (42%), and to help their children purchase a home (16%).

Twenty-four per cent of respondents in Ontario are likely to assist a child financially with the purchase of a home (29% in Toronto).

“Boomers who own property in Ontario have seen their equity grow while making memories in their family home. They want the same experience for their children and feel a sense of urgency, as prices are becoming more out of reach, to help get them on the property ladder,” said Heaps. “While competition is high across the province, Toronto remains a particularly difficult market to get into because of the higher price point. For some younger buyers, help from parents will determine whether they can purchase at all.”

Fifty-two per cent of boomer homeowners in Ontario said they would prefer to renovate their existing home rather than purchase another, and an additional 23 per cent said they would consider it.

For all regional and national responses, including Toronto, click here: rlp.ca/table_boomersurvey2021

Prairies (Saskatchewan and Manitoba)

Thirty-two per cent of boomers in the Prairies are considering purchasing a home within the next five years. Home ownership among boomers is higher than the national average with 78 per cent of Prairie boomers owning their own home, the majority of whom do not currently have a mortgage (66%). Twenty-one per cent of boomer homeowners in the region own more than one property, and 35 per cent have at least 50 per cent of their net wealth in real estate.

“I’ve seen many cases where boomers have moved to their secondary properties on the lake in retirement, but they don’t always sell their primary residences,” said Norm Fisher, broker and owner, Royal LePage Vidorra, in Saskatoon, Saskatchewan. “Home prices are more affordable in Saskatchewan, so established homeowners can afford to keep both.”

More than half (57%) of respondents in the Prairies said they would purchase a detached house if they were to buy, while 26 per cent said they would prefer an apartment/condominium.

“Most boomers are not eager to move into a significantly smaller space, but they do want a home that requires less maintenance, and won’t be a burden on their family or friends if they choose to spend several months away in the winter,” said Chris Pennycook, sales representative, Royal LePage Dynamic Real Estate, in Winnipeg, Manitoba.

Twenty-four per cent of boomers in the Prairies are likely to assist their children financially with the purchase of a home.

“I’ve been in real estate for 35 years. Young people getting financial help to buy their first home is not a new trend, but I can’t remember a time when parents, and in some cases grandparents, have helped this much,” added Pennycook.

Forty-one per cent of boomer homeowners in the Prairies said they would prefer to renovate their existing home rather than purchase another. An additional 31 per cent said they would consider it.

For all regional and national responses, click here: rlp.ca/table_boomersurvey2021

Alberta

Forty-one per cent of boomers in Alberta are considering purchasing a home within the next five years. At 84 per cent, Alberta has one of the highest rates of home ownership among boomers, the majority of whom do not currently have a mortgage (67%). Thirty-six per cent have at least 50 per cent of their net wealth in real estate. Twenty-four per cent of boomer homeowners in the province own more than one property.

“Owning a second property is common in Alberta as either a recreational property or as an investment. Real estate is highly affordable and has great value. You can buy a condo in Edmonton’s city centre as a student rental for less than $130,000,” said Tom Shearer, broker and owner, Royal LePage Noralta Real Estate, in Edmonton.

More than half (58%) of respondents in Alberta said they would purchase a detached house if they were to buy, while 13 per cent said they would prefer an apartment/condominium.

“Boomers in Calgary typically belong to one of two schools of thought: those who want to age in place if they can, and those who want to downsize into a bungalow or villa-style community,” said Corinne Lyall, broker and owner, Royal LePage Benchmark, in Calgary. “Downsizing does not necessarily mean moving into a condo. The preference for most is to have a smaller house with less maintenance.”

Of the 41 per cent of boomers in Alberta who say they are considering purchasing a primary residence in the next five years, 55 per cent say they would consider moving to a rural or recreational region. Seventeen per cent say they would consider purchasing a larger home than the one they currently reside in, 58 per cent would consider a similarly-sized property, and 66 per cent would consider downsizing. Respondents were able to choose more than one option. The most popular reason for downsizing is less home maintenance (70%). Other popular choices include the ability to free up money for things like retirement (36%), travel (28%), and to help their children purchase a home (6%).

Twenty-nine per cent of respondents in Alberta are likely to assist a child financially with the purchase of a home.

“Many boomers have built up significant wealth in real estate. It is common to see parents give financial gifts to adult children to help them own their own home nearby. This allows them to support each other, as often we see grandparents helping out with their grandkids,” added Shearer.

Nearly half (49%) of boomer homeowners in Alberta said they would prefer to renovate their existing home rather than purchase another, and an additional 24 per cent said they would consider it.

For all regional and national responses, click here: rlp.ca/table_boomersurvey2021

British Columbia

Thirty-nine per cent of boomers in British Columbia are considering purchasing a home within the next five years.

“Boomers are the most affluent generation in Canadian history and appreciate the equity they have built up in their homes,” said Caroline Baile, associate broker, Royal LePage Sussex, in North Vancouver. “While many did not have an immediate need to move due to additional space requirements, as safety restrictions are lifted and the vaccine roll-out is in full gear, many boomers will again think about their next move.”

Seventy-nine per cent of boomers in the province own their own home (73% in Vancouver), the majority of whom do not currently have a mortgage (66% and 64% in Vancouver). In B.C., 18 per cent of boomer homeowners currently own more than one property, and 48 per cent have at least 50 per cent of their net wealth in real estate, one of the highest rates of all regions surveyed in Canada.

More than half (54%) of respondents in B.C. said they would purchase a detached house if they were to buy, while 19 per cent said they would prefer an apartment/condominium.

“The trend we’re noticing among this group is rightsizing, rather than downsizing. They may choose a slightly smaller home, but they still want some outdoor space and room to entertain,” continued Baile. “Townhomes are very popular today among younger boomers, who aren’t quite ready for a condo but enjoy the freedom of a property with lower maintenance.”

Of the 39 per cent of boomers in B.C. who say they are considering purchasing a primary residence in the next five years, half say they would consider moving to a rural or recreational region. Thirty-six per cent say they would consider purchasing a larger home than the one they currently reside in, 64 per cent would consider a similarly-sized property, and 59 per cent would consider downsizing. Respondents were able to choose more than one option. The most popular reason for downsizing is less home maintenance (55%). Other popular choices include the ability to free up money for things like retirement (45%), travel (30%), and to help their children purchase a home (9%).

Thirty-one per cent of respondents in B.C. are likely to assist a child financially with the purchase of a home. That number jumps to 34 per cent in Vancouver.

Forty-five per cent of boomer homeowners in B.C. said they would prefer to renovate their existing home rather than purchase another, and an additional 27 per cent said they would consider it.

For all regional and national responses, including Vancouver, click here: rlp.ca/table_boomersurvey2021

Posted on

September 21, 2022

by

Marie & Kim Taverna

More than one in ten homeowners in Canada’s three largest urban centres owns multiple properties

Highlights:

According to a recent Royal LePage survey[1] of 1,500 homeowners in Canada’s three largest urban centres – Greater Toronto Area (GTA), Greater Montreal Area (GMA) and Greater Vancouver (GV) – more than ten per cent of Canadians polled currently own more than one property (13% in GTA, 12% in GMA, 14% in GV).

“While some secondary properties are used for recreational purposes, many of these homes are foundational to Canada’s critical supply of rental housing,” said Phil Soper, president and CEO, Royal LePage. “Entrepreneurial landlords supply housing to the thirty per cent of Canadians who rent, be they new immigrants, students, young people entering the labour force, or those who cannot or choose not to own their home.”

Twenty-one per cent of secondary property owners in the Greater Montreal Area say they used equity from their primary residence to complete the purchase. That number doubles (42%) in the greater regions of Toronto and Vancouver, where home prices are significantly higher.

When asked about the purpose of their secondary properties, more than two thirds of respondents in Greater Vancouver (65%) and the Greater Toronto Area (64%) said they were collecting rental income, if only some of the time. In the Greater Montreal Area, that number decreased to 35 per cent.

Witnessing home values across the country rising to new heights, younger Canadians who are financially able to purchase one home are confident in purchasing a secondary property as an investment. Eighteen per cent of homeowners aged 18 to 35 in the Greater Toronto Area own more than one property. In the Greater Montreal Area and Greater Vancouver, 16 per cent and 14 per cent of that age group own more than one property, respectively.

Greater Toronto Area

In the Greater Toronto Area, 27 per cent of secondary property owners said they were not collecting any rental income at all, while 49 per cent said they are using the unit solely as a rental property. Fifteen per cent said they were using the property some of the time and renting it out some of the time. Seven per cent of respondents said their secondary properties are currently vacant.

“Canadian homeowners believe in the value of real estate because they have seen their investments grow over time,” said Karen Millar, sales representative, Royal LePage Signature Realty. “People feel confident investing in real estate because it is a physical entity that they can experience. Although the market may see peaks and valleys, homes have historically generated wealth in the long run.”

In the Greater Toronto Area, 18 per cent of homeowners aged 18 to 35 currently own more than one property, while 11 per cent of homeowners over the age of 35 own more than one property.

“Young buyers are looking to capitalize on the real estate market by investing in a property that will appreciate over time. I have many younger clients who have purchased condos or smaller homes for as little as $300,000 outside of Toronto, in areas like Guelph and London, where the rental market is very active among students,” added Millar. “Parents of students in Ontario’s university towns are also taking advantage of the local rental market, purchasing a property – often times with multiple units – for their children to stay in while studying and also as a source of rental income from other students.”

A recent Royal LePage survey of Canadian boomers (chart), those born between 1946 and 1965, found that 54 per cent of the cohort in the Greater Toronto Area have at least half (50%) of their net wealth in real estate. Twenty-nine per cent say they have or would consider gifting or loaning money to a child to help with the purchase of a home. Another Royal LePage survey of Canadians aged 25 to 35 (chart) found that 93 per cent of the Torontonians in this age group consider home ownership a good financial investment.

Greater Montreal Area

In the Greater Montreal Area, where properties are more affordable than in the other two major urban centres surveyed, 37 per cent of secondary property owners said they were not collecting any rental income at all, while 25 per cent said they are using the unit solely as a rental property. Nine per cent said they were using the property some of the time and renting it out some of the time. Four per cent of respondents said their secondary properties are currently vacant.

“Among secondary property owners in Montreal, the majority are using the properties for leisure, like recreational purposes, rather than as an investment,” said Roseline Guèvremont, real estate broker, Royal LePage Tendance. “In Toronto and Vancouver, where prices have been soaring for several years, homeowners have been taking advantage of the significant equity in their primary residences in order to purchase a secondary property, and renting it out at least part of the time as an investment. In Montreal, although the real estate market has begun to catch up in recent years, prices remain considerably more affordable, so buyers can purchase without necessarily leveraging equity from a primary residence.”

In the Greater Montreal Area, 16 per cent of homeowners aged 18 to 35 currently own more than one property, while 11 per cent of homeowners over the age of 35 own more than one property.

Guèvremont noted that younger buyers are becoming more and more interested in owning property, whether to improve their quality of life, to generate new sources of revenue, or to have new experiences.

“Confidence in the Montreal real estate market has continued to rise in recent years, and many clients have expressed to me their preference to invest in brick and mortar properties. For younger buyers, it’s much more straightforward than investing in the stock market.

“With the return of in-person classes this fall and the opening of the border to U.S. visitors, demand is already being renewed in the rental market,” said Guèvremont. “Montreal’s real estate investors had a tough time generating profits from their units over the last year due to COVID-19.”

A recent Royal LePage survey of Canadian boomers (chart), those born between 1946 and 1965, found that 41 per cent of the cohort in the Greater Montreal Area have at least half (50%) of their net wealth in real estate. Twenty-four per cent say they have or would consider gifting or loaning money to a child to help with the purchase of a home. Another Royal LePage survey of Canadians aged 25 to 35 (chart) found that 92 per cent of Montrealers in this age group consider home ownership a good financial investment.

Greater Vancouver

In Greater Vancouver, 27 per cent of secondary property owners said they were not collecting any rental income at all, while 51 per cent said they are using the unit solely as a rental property. Thirteen per cent said they were using the property some of the time and renting it out some of the time. Seven per cent of respondents said their secondary properties are currently vacant.

“Real estate is an integral part of retirement planning for many Vancouver homeowners,” said Caroline Baile, real estate broker, Royal LePage Sussex. “While some are using their secondary properties, possibly a cottage or a ski chalet, many of those with multiple homes are looking to build future equity as a means of sustaining a desired lifestyle down the road. Investment properties are not likely being used to subsidize monthly income, but are seen as a long-term investment.”

In Greater Vancouver, the country’s most expensive city to buy real estate, 14 per cent of homeowners aged 18 to 35 currently own more than one property. Similarly, 14 per cent of homeowners over the age of 35 own more than one property.

“Younger Canadians are sitting in the driver’s seat of their own futures. They are very business savvy, and have a clear idea of what they want their retirement years to look like. Young people today put a lot of emphasis on work-life balance. They want their money to work for them, and they recognize that investing in real estate has the potential for great returns,” continued Baile. “While so many young Canadians struggle to enter the real estate market, those fortunate enough to do so, whether on their own or with financial support from their parents, will reap the benefits in the future.”

Posted on

September 21, 2022

by

Marie Taverna

Six in ten non-homeowner millennials in Canada believe they will one day own a home, but half say they would have to relocate: Royal LePage Survey

Survey highlights:

–According to a recent Royal LePage survey[1], conducted by Leger, 60 per cent of Canadian millennials, people aged 26 to 41, who do not currently own a home believe they will one day. Of them, however, 52 per cent say they would have to relocate in order to achieve this milestone; one their parents seem to have reached with greater ease. Canada’s chronic housing supply shortage continues to challenge buyers of every age, especially those looking to enter the market.

When broken out by age, 62 per cent of respondents under the age of 35 say they believe they will own a home one day, compared to 56 per cent of those aged 35 and up. Meanwhile, 25 per cent of non-homeowner millennials across the country do not believe they will ever own a home.

“Many Canadians who are in the stage of life where homebuying is a top priority, especially younger millennials, remain committed to achieving home ownership and are optimistic about the opportunities that lie ahead, due in large part to the example of their parents and family members who have reaped the benefits of our nation’s historically strong real estate market,” said Phil Soper, president and CEO, Royal LePage. “Currently the largest proportion of our population, and so arguably the most impactful, millennials are a resilient group who are willing to make the necessary sacrifices in order to reach this milestone.”

According to the survey, 57 per cent of Canadian millennials are already homeowners. That figure is higher among those aged 35 and up (63%). And, 51 per cent of the cohort plan to purchase a home within the next five years – whether their first home, a move-on property or a secondary residence – which means more than 4 million[2] young Canadians will be looking to make a purchase between now and 2027. Almost half of them (45%) will be first-time homebuyers. Of the millennials who plan to buy their first home or sell their current home and move within this period, 47 per cent say they will remain in their current city or town, while 41 per cent say they plan to relocate.

“The need for a significant increase in the supply of housing in Canada has not gone away. While we are currently seeing a slowdown in market activity, as prospective buyers temporarily put their home purchase plans on pause while they seek to understand the full impact of rising interest rates and inflation on their bottom line, we expect that activity will rise again, although not at the same rate we saw throughout 2021 and early 2022. The return of these sidelined purchase intenders, a growing population, largely from increased immigration levels, together with household formation changes – individual households made up of boomer parents and their millennial children evolving into two, three or four households – will require more available housing stock to ensure a balanced market and to help bring affordability back within reach of many Canadians,” continued Soper.

Competition for properties and the prevalence of multiple-offer scenarios may have eased in recent months, however, young buyers continue to face significant challenges, as the cost of borrowing has become a barrier to affordability for many first-time buyers.

“Policy makers should take note that between millennial demand, immigration and the growing pipeline of those who could not transact over the last two years, more supply is required. We could see another surge in price appreciation, following short-term economic softening, when these sidelined purchase intenders transact.”

According to the survey, of the millennials in Canada who do not own a home, 68 per cent feel that home ownership is important. That figure is higher among those under the age of 35 (72%).

“While affordability remains a challenge, Canada continues to see strong demand from millennials who, like their parents, see home ownership as a right of passage. The desire to be a homeowner remains strong among Canadians of all ages. Despite the harsh reality many young people are facing – that buying their first home today is more difficult than it was for their parents – the majority still value home ownership and see it as a long-term investment in their futures,” said Soper.

In a 2021 survey of Canadian boomers, Royal LePage found that 25 per cent of those aged between 57 and 76 would help, or have already helped, their children financially with the purchase of a property[3].

When it comes to relocation, 72 per cent of millennials in Canada say that if the cost of living was not an issue, they would choose to continue living in their current city or town. However, 46 per cent do not believe their salaries will increase at a rate that will allow them to buy a home in their current location. This result appears to be reflective of lifestyle choice, rather than proximity to their place of work. Forty per cent of millennials say they would change employers to be able to work fully remotely. The top motivators for wanting to work from home are high commuting costs, long commuting times and traffic, and the ability to manage household duties while working from home.

“Employment and migration trends have intersected with real estate market trends over the last two years. The irreversible impact that the pandemic has had on our workforce and the manner in which employees do their jobs sparked a shift in the mentality of many Canadians, especially young professionals, who are reprioritizing their lives and their plans for the future,” said Soper. “Strong real estate demand is no longer concentrated in the major centres, but has expanded to many suburbs and exurbs where homebuyers can purchase larger, more affordable properties, as the tolerance for commuting wanes and the desire to have more flexibility in the hours and location one works increases.”

Twenty per cent of millennials in Canada say their ideal work/life scenario would be to live outside the city and work fully remotely; the most popular answer of all options offered. The second most popular option is to live in the city and work fully remotely (14%).

Royal LePage 2022 Demographic Survey: Canadian Millennials – Data chart:rlp.ca/table_2022-millennials-report

Posted on

September 18, 2022

by

Marie Taverna

Metro Vancouver’s housing market sees fewer home buyers and sellers in August

Metro Vancouver’s housing market is experiencing a quieter summer season marked by reduced sale and listing activity.

The Real Estate Board of Greater Vancouver (REBGV) reports that residential home sales in the region totalled 1,870 in August 2022, a 40.7 per cent decrease from the 3,152 sales recorded in August 2021, and a 0.9 per cent decrease from the 1,887 homes sold in July 2022.

Last month’s sales were 29.2 per cent below the 10-year August sales average.

“With inflationary pressure and interest rates on the rise, home buyer and seller activity shifted below our long-term seasonal averages this summer,” Andrew Lis, REBGV’s director, economics and data analytics said. “This shift in market conditions caused prices to edge down over the past four months.”

There were 3,328 detached, attached and apartment properties newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in August 2022. This represents a 17.5 per cent decrease compared to the 4,032 homes listed in August 2021 and a 16 per cent decrease compared to July 2022 when 3,960 homes were listed.

The total number of homes currently listed for sale on the MLS® system in Metro Vancouver is 9,662, a 7.3 per cent increase compared to August 2021 (9,005) and a 6.1 per cent decrease compared to July 2022 (10,288).

“Home buyers and sellers are taking more time to assess what this changing landscape means for their housing needs,” Lis said. “Preparation is critical in today’s market. Work with your Realtor to assess what today’s home prices, financing options, and other considerations mean for you.”

For all property types, the sales-to-active listings ratio for August 2022 is 19.4 per cent. By property type, the ratio is 12.2 per cent for detached homes, 25.3 per cent for townhomes, and 24.8 per cent for apartments.

Generally, analysts say downward pressure on home prices occurs when the ratio dips below 12 per cent for a sustained period, while home prices often experience upward pressure when it surpasses 20 per cent over several months.

The MLS® Home Price Index composite benchmark price for all residential properties in Metro Vancouver is currently $1,180,500. This represents a 7.4 per cent increase over August 2021 and a 2.2 per cent decrease compared to July 2022.

Sales of detached homes in August 2022 reached 517, a 45.3 per cent decrease from the 945 detached sales recorded in August 2021. The benchmark price for a detached home is $1,954,100. This represents a 7.9 per cent increase from August 2021 and a 2.3 per cent decrease compared to July 2022.

Sales of apartment homes reached 998 in August 2022, a 38.8 per cent decrease compared to the 1,631 sales in August 2021. The benchmark price of an apartment home is $740,100. This represents an 8.7 per cent increase from August 2021 and a two per cent decrease compared to July 2022.

Attached home sales in August 2022 totalled 355, a 38.4 per cent decrease compared to the 576 sales in August 2021. The benchmark price of an attached home is $1,069,100. This represents a 12.7 per cent increase from August 2021 and a 2.5 per cent decrease compared to July 2022.

Download the August 2022 stats package.

Posted on

September 18, 2022

by

Marie Taverna

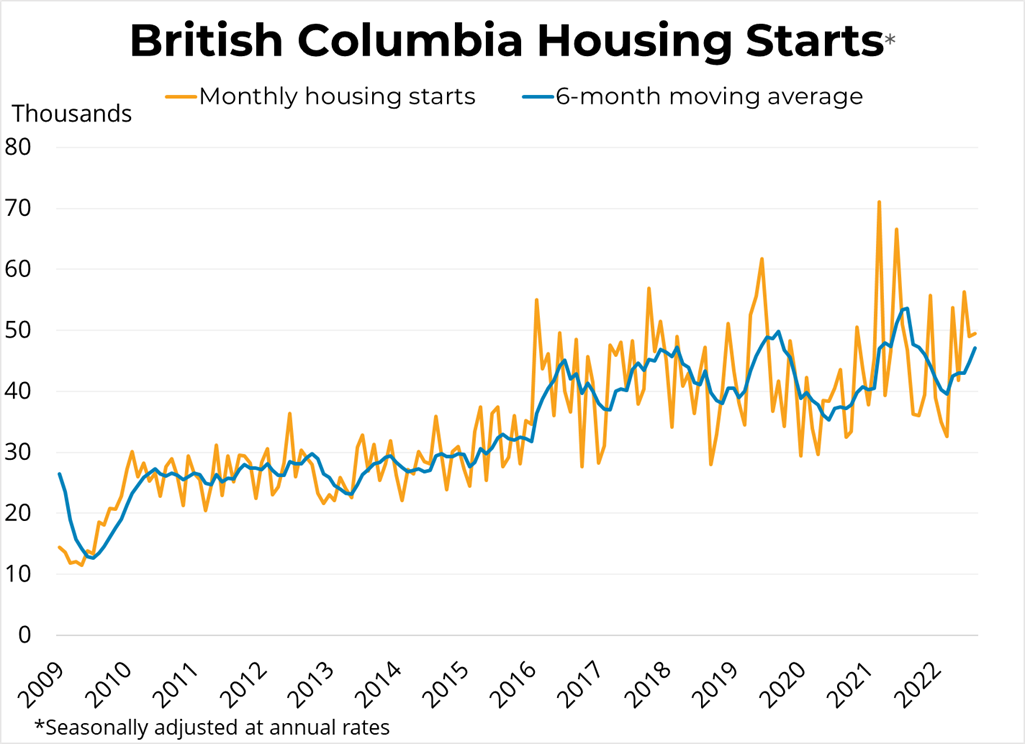

Canadian Housing Starts (August 2022) - September 16, 2022

|

|

Canadian housing starts fell by 7.7k (2.8 per cent) to 267.4k units in August at a seasonally-adjusted annual rate (SAAR). Comparing year-over-year, starts were up from August of 2021 (2.5 per cent). Single-detached housing starts rose 1 per cent to 73.4k, while multi-family and others declined 4.2 per cent to 194k (SAAR).

In British Columbia, starts increased by 0.8 per cent in August, rising to 49.5k units SAAR in all areas of the province. In areas in the province with 10,000 or more residents, single-detached starts fell 6.7 per cent m/m to 6.7k units while multi-family starts rose 1.6 per cent to 39k units. Starts in the province were 5.7 per cent above the levels from August 2021. Starts were flat month over month in Vancouver, up by 6.5k in Kelowna, and down by 1.3k in Abbotsford and 6.8k in Victoria. The 6-month moving average trend rose 5.4 per cent to 47.1k in BC in August.

Link: https://mailchi.mp/bcrea/canadian-housing-starts-august-2022 |

|

|

Posted on

May 5, 2022

by

Marie Taverna

Metro Vancouver home sales return to more traditional levels in April

Home buyer demand in Metro Vancouver* returned to more historically typical levels in April.

The Real Estate Board of Greater Vancouver (REBGV) reports that residential home sales in the region totalled 3,232 in April 2022, a 34.1 per cent decrease from the 4,908 sales recorded in April 2021, and a 25.6 per cent decrease from the 4,344 homes sold in March 2022.

Last month’s sales were 1.5 per cent above the 10-year April sales average.

“So far this spring, we’ve seen home sales ease down from the record-breaking pace of the last year,” Daniel John, REBGV Chair said. “While a small sample size, the return to a more traditional pace of home sales that we’ve experienced over the last two months provides hopeful home buyers more time to make decisions, secure financing and perform other due diligence such as home inspections.”

There were 6,107 detached, attached and apartment properties newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in April 2022. This represents a 23.1 per cent decrease compared to the 7,938 homes listed in April 2021 and an 8.5 per cent decrease compared to March 2022 when 6,673 homes were listed.

The total number of homes currently listed for sale on the MLS® system in Metro Vancouver is 8,796, a 14.1 per cent decrease compared to April 2021 (10,245) and a 15.3 per cent increase compared to March 2022 (7,628).

“With interest rates climbing and the total inventory of homes for sale inching higher, it’s important to work with your local Realtor to understand how these factors could affect your home buying or selling situation,” John said.

For all property types, the sales-to-active listings ratio for April 2022 is 36.7 per cent. By property type, the ratio is 25.3 per cent for detached homes, 47.1 per cent for townhomes, and 45 per cent for apartments.

Generally, analysts say downward pressure on home prices occurs when the ratio dips below 12 per cent for a sustained period, while home prices often experience upward pressure when it surpasses 20 per cent over several months.

The MLS® Home Price Index composite benchmark price for all residential properties in Metro Vancouver is currently $1,374,500. This represents an 18.9 per cent increase over April 2021 and a one per cent increase compared to March 2022.

Sales of detached homes in April 2022 reached 962, a 41.9 per cent decrease from the 1,655 detached sales recorded in April 2021. The benchmark price for a detached home is $2,139,200. This represents a 20.8 per cent increase from April 2021 and a one per cent increase compared to March 2022.

Sales of apartment homes reached 1,692 in April 2022, a 26.1 per cent decrease compared to the 2,289 sales in April 2021. The benchmark price of an apartment home is $844,700. This represents a 16 per cent increase from April 2021 and a 1.1 per cent increase compared to March 2022.