Subscribe with RSS Reader

Subscribe with RSS ReaderRoyal Lepage By The Numbers October 2024

Royal Lepage By The Numbers October 2024

Posted on

November 14, 2024

by

Marie Taverna

DROP OFF YOUR BLANKETS AND WARM CLOTHING TODAY

Posted on

November 14, 2024

by

Marie Taverna

Wallet-Wise and Warm: How to Save on Heating Bills

Posted on

November 5, 2024

by

Marie Taverna

Lung Cancer Awareness Month: Radon

Posted on

November 5, 2024

by

Marie Taverna

Cozying Up Your Outdoor Oasis

Posted on

November 5, 2024

by

Marie Taverna

MARKET UPDATE October

Posted on

November 5, 2024

by

Marie Taverna

Ways to lower your heating bill this winter

Posted on

November 5, 2024

by

Marie Taverna

Greater Vancouver Housing Stats for October

Posted on

November 5, 2024

by

Marie Taverna

U.S. web traffic spikes on royallepage.ca in lead up to 2024 presidential election

Posted on

November 4, 2024

by

Marie Taverna

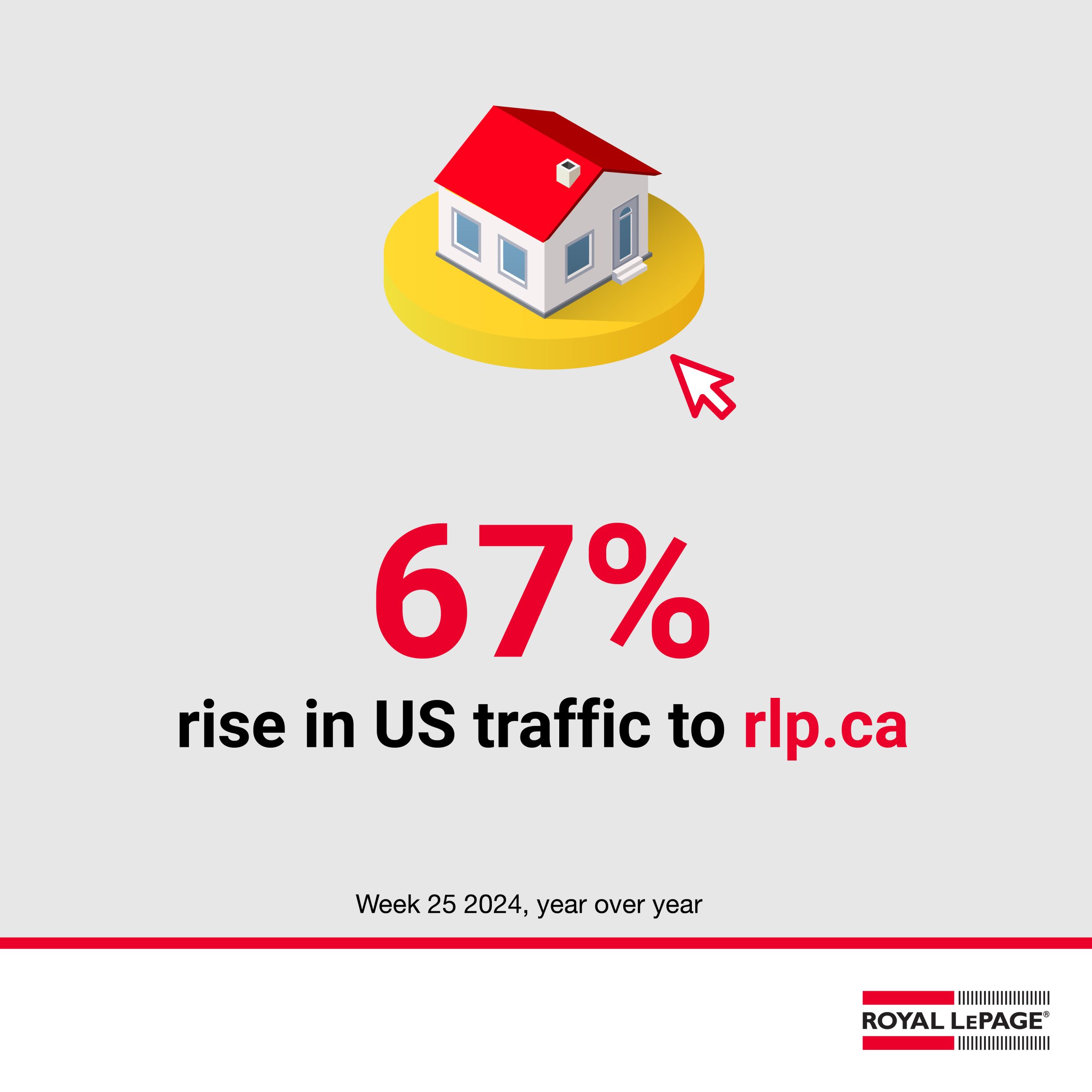

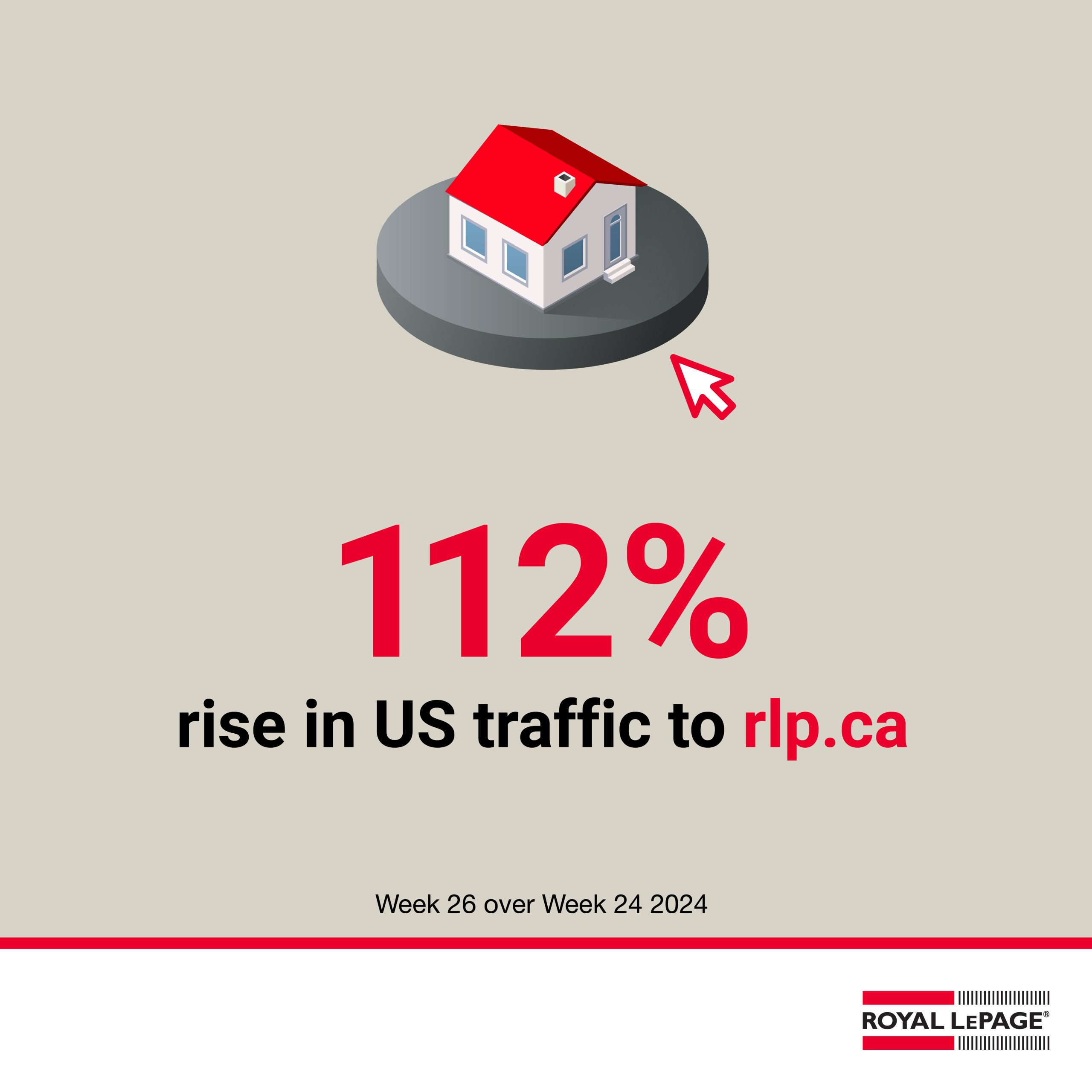

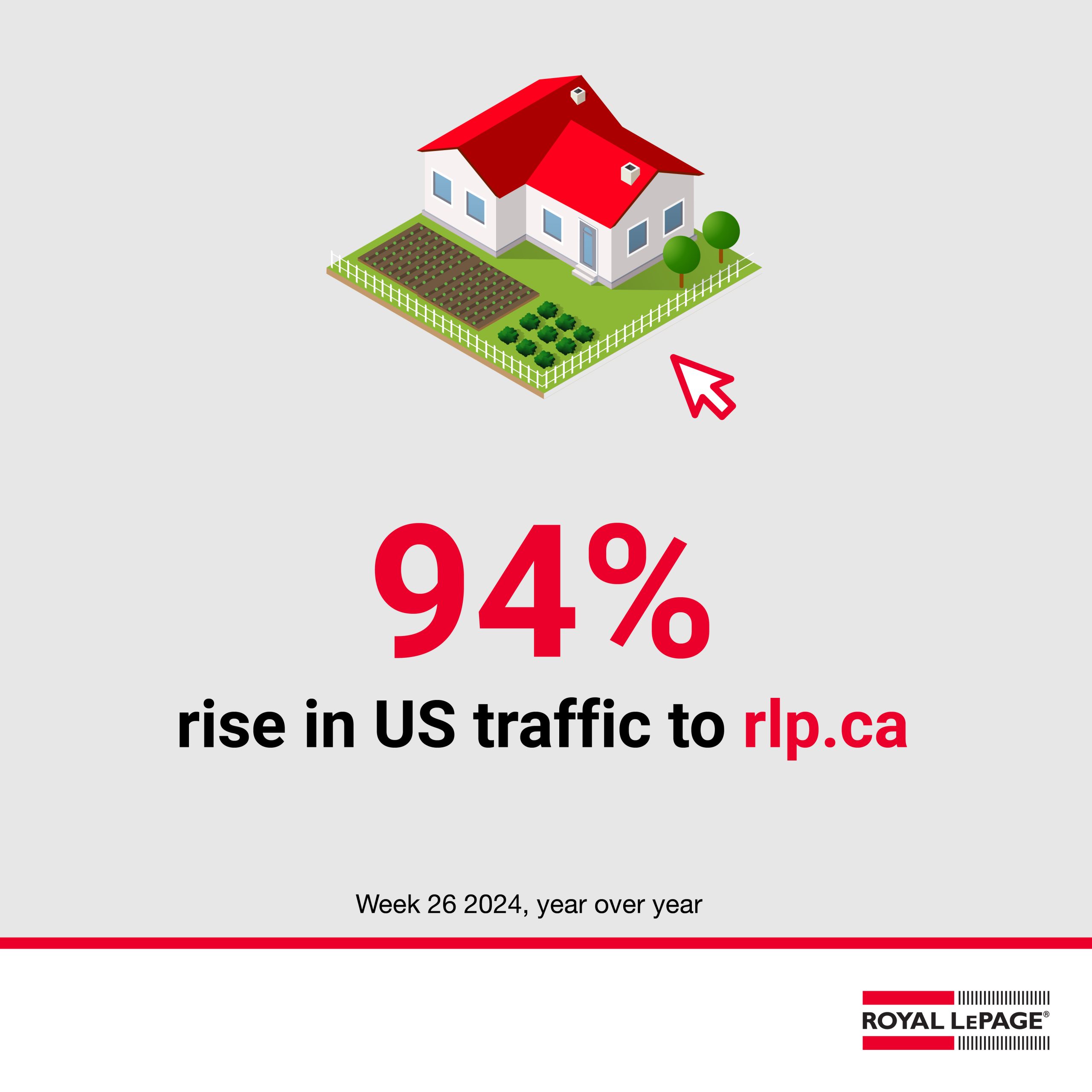

Millions of Americans will head to the polls next week to elect a new president. It appears some are considering relocation to Canada if the outcome of the election is not in their favour. According to data released today by Royal LePage®, visits by Americans to royallepage.ca – the company’s consumer real estate portal and the most-visited real estate company website in Canada – have risen significantly since the U.S. presidential election unofficially kicked off this summer. After months of typical web traffic from our neighbours to the south, U.S.-originated sessions to royallepage.ca more than doubled, surging 104 per cent week over week (67% year over year) in the week of June 16th (Week 25). The following week, on the heels of the first presidential debate between President Joe Biden and then-presumptive Republican nominee, Donald Trump, traffic peaked with an additional 4 per cent increase in visitors over the week prior (112% over week 24 and 94% year over year). There have been elevated levels of traffic from U.S. visitors ever since.     “Consistently ranking as one of the best countries in the world to live in, Canada continues to be a significant destination for international relocation; a fact unlikely to change in the years ahead,” said Phil Soper, president and chief executive officer, Royal LePage. “Canada’s relative political and social stability, high quality of life, and access to education and universal healthcare, make it a highly attractive country for newcomers from Europe, Asia and around the world. For Americans, the transition is even easier, considering the proximity and lack of a language barrier in most provinces.” July 2024 recorded the highest web traffic on royallepage.ca from U.S. visitors over the past 12 months, with a noticeable single-day spike recorded on July 15th – the same day former president Donald Trump officially became the Republican nominee for the 2024 presidential election. This was also just two days after the first attempt on his life, which occurred during a rally in Pennsylvania. This is not the first time Americans’ interest in Canada has been linked to U.S. political events. In 2017, a similar report found U.S. web traffic to royallepage.ca skyrocketed, jumping a massive 329 per cent the day following the 2016 election, and climbing 210 per cent year over year the week after Donald Trump’s electoral victory.1 “Americans are a minority in the hundreds of thousands of new Canadians we welcome each year, yet around presidential election time, they get very, very interested in their neighbour to the north. Nothing like political and economic uncertainty to get people searching for greener grass!” noted Soper. “Browsing online listings and moving to another country are two entirely different matters – given the rigorous application process and the federal government’s recent decision to reduce immigration targets, only serious and qualified candidates will actually relocate.” The Government of Canada announced that it would be lowering its permanent resident targets for the next three years, reducing 2025 levels by more than 20%.2 Regional trendsAmong the ten most common states from which American visitors to royallepage.ca hail, most are blue states – meaning a majority of voters in the state voted for the Democratic Party candidate. However, since June 2024, the region with the highest number of visitors has consistently been the historically Republican state of South Carolina. From June through September, American interest in Canadian real estate was concentrated in the country’s largest markets, with Ontario, British Columbia and Quebec receiving 70 per cent of all regional pageviews generated by U.S. visitors on royallepage.ca. Ontario led the country in American searches during this time, with 38 per cent of regional searches, followed by B.C. (17%) and Quebec (16%). “Just as Canadians love U.S. sun states, American citizens have historically played an important role in recreational property markets across Canada. Given today’s polarized American political landscape and the divisive nature of this election, it would not be surprising if interest from America shifted from vacation homes to more permanent opportunities,” said Soper. Voters in the United States will head to the polls on November 5th to elect their next president. 1U.S. Interest in Canadian Real Estate Surges Following U.S. Presidential Election, January 20, 2017 2Government of Canada reduces immigration, October 24, 2024 ContributorAnne-Elise Cugliari AllegrittiDirector of Communications, Royal LePage Mortgage Reforms

Posted on

October 31, 2024

by

Marie Taverna

Housing Monitor Dashboard - October 29, 2024

Posted on

October 31, 2024

by

Marie Taverna

About BCREA’s Housing Monitor DashboardThe BCREA Economics team has created the Housing Monitor Dashboard to help REALTORS®monitor BC’s housing market. This dashboard, which is updated monthly, provides up-to-date data on key variables for public education and use. Focuses include:

In thedashboard, the image and data are available for download under each chart, where possible. "Copyright British Columbia Real Estate Association. Reprinted with permission." BCREA makes no guarantees as to the accuracy or completeness of this information. 10 Horrifying Home Design Trends: 2024 Edition

Posted on

October 31, 2024

by

Marie Taverna

From the latest DIY hashtag on social media to style themes prepackaged as a design “core,” home design fads tend to die quickly. But until trends like “Yeehaw Core” meet their final demise, we’re here to wish them dead. The Styled Staged & Sold blog does an annual countdown of the worst home design trends of the year. Last year, the trends that earned a place on our list included out-of-place blob furniture, blindingly shiny surfaces and uncomfortable dining benches. So, what new frights have emerged this year? Here are some of the most haunting home styles of the year. Be sure to chime in below with the styles that are giving you the creeps! 10. Open shelving in the kitchen Photo credit: Brizmaker / Getty Images By now, some homeowners undoubtedly are missing their upper kitchen cabinets. The pressure involved with open shelving likely has worn thin: keeping dishes pristinely displayed and organized—and the constant dusting! Certainly, open shelves in lieu of upper cabinets can work in small kitchens if you need to trick the eye to make the space seem larger. But in most kitchens, cabinets are beloved by homeowners for their organizational sanity. It’s just a bonus when they look nice, too. 9. Black fixtures on all-white interiors Photo credit: Joe Hendrickson / Getty Images Matted black finishes may be drawing too much of the focus, particularly in an otherwise all-white room. Black faucets and knobs can end up stealing the spotlight, but is that really what you want guests to focus on? Faucets don’t sell homes. 8. Cramped garages Photo credit: UCpage / Getty Images Big houses with small garages are impractical. Vehicles have gotten larger, and households have accumulated more and more stuff. Yet, garage space is shrinking. From the 1960s to the 2000s, the average standardized two-car garage grew to 24x24 feet. Lately, builders are constructing homes with garages that are 20x20 feet. That can make for a tight squeeze considering an average pickup truck is more than 19 feet in length and a minivan can stretch to 18 feet. With smaller lots to contend with, builders are favoring larger interiors over garage space. But cramped garages mean homeowners are shimmying out of their parked car or even parking on the driveway or street. 7. All-gray interiors Photo credit: NelleG / Getty Images Shades of gray have been blanketing our homes, from walls and floors to furniture, carpeting, rugs, paint, accessories and more. It’s all starting to feel cold and dreary. Even Dorothy from “The Wizard of Oz” eventually woke up to some color—and it’s time we do, too! The latest trend is clear: Color brightens up our spaces. Lately, contrasting colors and patterns have become a way to beat the gray. 6. The oversized, supersized shower Photo credit: Melissa Tracey Seriously, how big is too big for a shower? We may have reached the tipping point. Even bath tubs are now being added inside these supersized showers, known as “wetrooms.” And some homeowners are even adding plants inside their shower for added décor. (A shower greenhouse—why not?) With big showers has come the need for more faucets and sprays that surround all sides, which can make it seem more like a powerful car wash than a relaxing spa. The time may have finally come to dial back the shower remodels to a more practical size. You’ll save money, too! 5. Overpainting with white Photo credit: Plus69 / Getty Images White trim, white-painted brick houses and white doors. We’ve all subscribed to the same design playbook: When in doubt, paint it white! More homeowners are starting to question that logic. Colored trim is “in” and so are brightly colored doors. Wood tones are beginning to shine through once again, too. Don’t assume that older, red or brown brick exteriors or fireplaces always must be painted white to feel fresh or modern. Once you paint it, you can never go back! White can be tough to keep clean and often requires a lot of upkeep. Some regret over white paint is likely brewing. 4. Mosaic tile accent strips Photo credit: Joe Hendrickson / Getty Images Colorful rectangular or square glass tiles were once a popular backsplash trend in the early 2000s, but designers now call it outdated. The tile accent strips often include a mixture of different colors and can look very busy and cramped. Instead, backsplashes are going big, featuring larger format tiles or stone slabs that cascade up the wall. Fewer grout lines can offer a more modern, clean finish. 3. Stainless steel kitchens Photo credit: Scott Van Dyke / Getty Images This trend went out as quickly as it came in, and most of us saw it coming. Keeping a stainless steel refrigerator smudge-proof is difficult enough; imagine having to keep shiny metal shelves and stainless steel backsplashes spotless, too! Popular cooking shows like “Boiling Point” and “The Bear” may have helped propel this kitchen design trend, but we’ll happily leave this one to the chefs. 2. TikTok DIY home trends Photo credit: SB Arts Media “I found this great home idea on TikTok!” This statement alone should sound the alarm on an incoming design faux pas. Consider, some of these once-trending ideas:

TikTok has become a popular place for serving up videos on DIY home projects meant to inspire us. But sometimes, these so-called great ideas can borderline on disastrous, if not dangerous, for your home. 1. Design-cores Photo credit: Stocknroll / Getty Images Cluttercore, Cottagecore, Grandpacore, Fantasycore, Yeehaw Core—and yes, Barbiecore. Likely the most hyped of these, Barbiecore had the longest rein of these core-styles, but taking home inspiration from a plastic doll was never to last past childhood. Design trends that get labeled as a design “core” tend to be an overly themed style that will likely fade as fast as an Instagram story. Encapsulate these fads in a Pinterest folder if you must. We’ll all surely laugh about them later! Over-the-top design themes that try to imitate Barbie, grandpa or the Wild West can look off-putting in real life. Instead, fit your home’s style to your individual tastes—and keep grandpa out of it. After all, just like an apple core, these cores tend to rot fast. Don’t let a design core stink up your home. What do you think? What are the scariest design trends you’ve been spotting in 2024 and that you hope will fade in the new year? BCREA ECONOMICS

Posted on

October 31, 2024

by

Marie Taverna

|

|

|

The arrival of storms Beryl and Debby brought record rainfall to many parts of Quebec and Ontario in the summer of 2024. Unprecedented flood damage is forcing municipalities and other levels of government to rethink their infrastructures, as extreme weather events occur with increasing frequency. But while we wait for solutions to be put in place to limit the damage to city water systems, here are some ideas to help you better protect your home from future flooding.

There are many consequences. In addition to immediate material damage, there is an increased risk of structural deterioration, mold and loss of property value. Furthermore, insurance could become more expensive or more difficult to obtain for homes located in high-risk areas. Homeowners must therefore anticipate these risks and adopt preventive measures to protect their investment.

With a significant increase in torrential rains and overflows in urban areas, it’s crucial to manage water pipes in the basement. First of all, if your home is flooded, the first thing to do is diagnose the problem at its source, to understand how and where the water has infiltrated, so you can take the appropriate corrective measures.

Installing backflow prevention valves, which ensure that sewage does not flow back up the pipes, is an essential first step. However, sometimes these are not enough. To ensure a superior seal, it is best to install double check valves in the basement. Also ensure that sump pumps are working properly to help eliminate stagnant water around the foundation.

Checking gutters and drains is another important preventive step you can take in the spring and fall to make sure they’re not clogged and that water is draining as far away from the foundation as possible. Make sure your gutters have extensions, so that water doesn’t pool around the property.

In some cases, grading of the ground around the property is considered, so that water runs towards the street and not the property. The aim is to keep as much water as possible from stagnating near the foundation. In addition, installing drainage curbs around windows located close to the ground is an excellent way of preventing water from seeping in.

In the medium term, it’s a good idea to invest in a regular inspection of your home by a professional, whether a building inspector or a plumber. These experts can detect potential faults in foundations, water pipes or drainage systems. Proactively repairing these problems can make a big difference in the event of flooding. Moreover, knowing your property and its level of risk in the event of water infiltration can help you anticipate problems and give confidence to a future buyer, for example.

In the long term, choosing the right location for your home is of paramount importance. If you’re in the buying process, find out about the neighbourhood’s flooding history. If you’re already a homeowner, consider landscaping work to raise the ground around the house or improve drainage. It’s also advisable to consult an engineer or building inspector to assess the feasibility of such modifications.

We’ve seen once again this year that no one is immune. Floods are no longer limited to homes in flood-prone areas. They can affect any municipality, any neighbourhood. It’s becoming imperative for citizens, cities and insurers to work together to prepare for this new era of climate change. Everyone must play their part, whether by adopting preventive measures or adapting infrastructures.

For the first time in two years, the Bank of Canada’s overnight lending rate has hit under 4%.

In its scheduled October 2024 announcement, the central bank lowered the target for the overnight lending rate by 50 basis points to reach 3.75%. This marks the fourth consecutive cut to rates in 2024, and the largest decrease since the onset of the pandemic in March 2020.

In September, Canada’s Consumer Price Index recorded the smallest yearly increase since February 2021, rising 1.6% year over year, hitting under the Bank’s 2% inflation target for the second consecutive month. This was a key factor in the Bank’s decision to lower the lending rate by a larger amount in October.

“In the past few months, inflation has come down significantly from 2.7% in June to 1.6% in September. Recent indicators suggest it will be around 2% in October. Price pressures are no longer broad-based, and both our measures of core inflation are now under 2.5%. Our surveys also find that business and consumer expectations of inflation have shifted down and are nearing normal. All this suggests we are back to low inflation. This is good news for Canadians,” said Tiff Macklem, Governor of the Bank of Canada, in a press conference with reporters following the announcement.

“If the economy evolves broadly in line with this forecast, we anticipate cutting our policy rate further to support demand and keep inflation on target. The timing and pace of further interest rate cuts will depend on incoming information and our assessment of its implications for the inflation outlook. We will take our monetary policy decisions one at a time,” he added.

Another cut to the overnight lending rate may be enough to stimulate activity in stagnant housing markets across Canada come spring, especially among buyers who have been sidelined by the higher cost of borrowing over the past two years.

In its Q3 2024 Home Price Update & Market Forecast, Royal LePage predicted that the aggregate price of a home in Canada will increase 5.5% in the fourth quarter of 2024, compared to the same quarter last year. As lower interest rates boost consumer confidence and borrowing power, home prices are expected to increase as more buyers re-enter the market. Rising demand in the late months of 2024 and into the new year will likely put Canada’s housing market on track for an early spring market.

“Activity in Canada’s housing market has been sluggish in many regions due to higher borrowing costs, but today’s more aggressive cut to lending rates could cause the tide to turn quickly. For those with variable rate mortgages – who will benefit from the rate drop immediately – or those with fast-approaching loan renewals, today’s announcement is welcome news indeed,” said Phil Soper, president and CEO of Royal LePage. “With every cut to the overnight lending rate, more homebuyers are expected to come off of the sidelines. In turn, rising demand will cause home prices to increase more rapidly, eliminating the advantages of lower borrowing costs. We expect that an early spring market is on the cards – a pull-ahead trend we’ve seen in previous market turnarounds.”

Though the Bank of Canada started to reduce rates in June, many homebuyers have been waiting for a more substantial cut to rates before choosing to reboot their purchase plans. According to a Royal LePage survey, conducted by Leger, 51% of Canadians who put their home buying plans on hold the last two years said they would return to the market when the Bank of Canada reduced its key lending rate. Eighteen percent said they would wait for a cut of 50 to 100 basis points, and 23% said they’d need to see a cut of more than 100 basis points before considering resuming their search.

The Bank of Canada will make its next interest rate announcement on Wednesday, December 11th, the last announcement for 2024.

Read the full October 23rd report here.

Communications manager, Royal LePage

Michelle is a member of Royal LePage’s Communications and Public Relations team, and works to deliver unique and insightful Canadian real estate content to media and consumers. Prior to joining Royal LePage, Michelle was an online reporter specializing in Canadian real estate and pre-construction development. She is a graduate of Toronto Metropolitan University’s esteemed journalism program.

|

|

Today, the Bank of Canada dropped the overnight lending rate by 50 basis points to 3.75%, marking the fourth consecutive cut to rates in 2024, and the largest decrease since the onset of the pandemic in March 2020.

For many homebuyers, this may be the signal needed to move off of the sidelines and into the market. As lower interest rates boost consumer confidence and borrowing power, home prices are expected to rise as more buyers reignite their purchase plans.

Want to know more about how the Bank of Canada announcement will impact the market? Read more in the latest post on the RLP blog:

https://blog.royallepage.ca/bank-of-canada-update.../

Stay tuned for the next announcement on December 11.

#RoyalLePage #RLP #Canada #InterestRates #BankofCanada #Mortgage #HousingMarket

|

|

|

|

|

|

|

|

Let's discuss your next home sale or purchase, with no obligation.

Give me a call at 604-802-7759